Knowledge-oriented firms keep expanding economic output

Tech and AI innovators in San Francisco and elsewhere have developed tools to make knowledge workers much more productive, but further leaps could present a downside risk to future office demand. (Anthony Lindsey/CoStar)

By Phil Mobley via CoStar

CoStar Analytics

February 23, 2026 | 12:09 P.M.

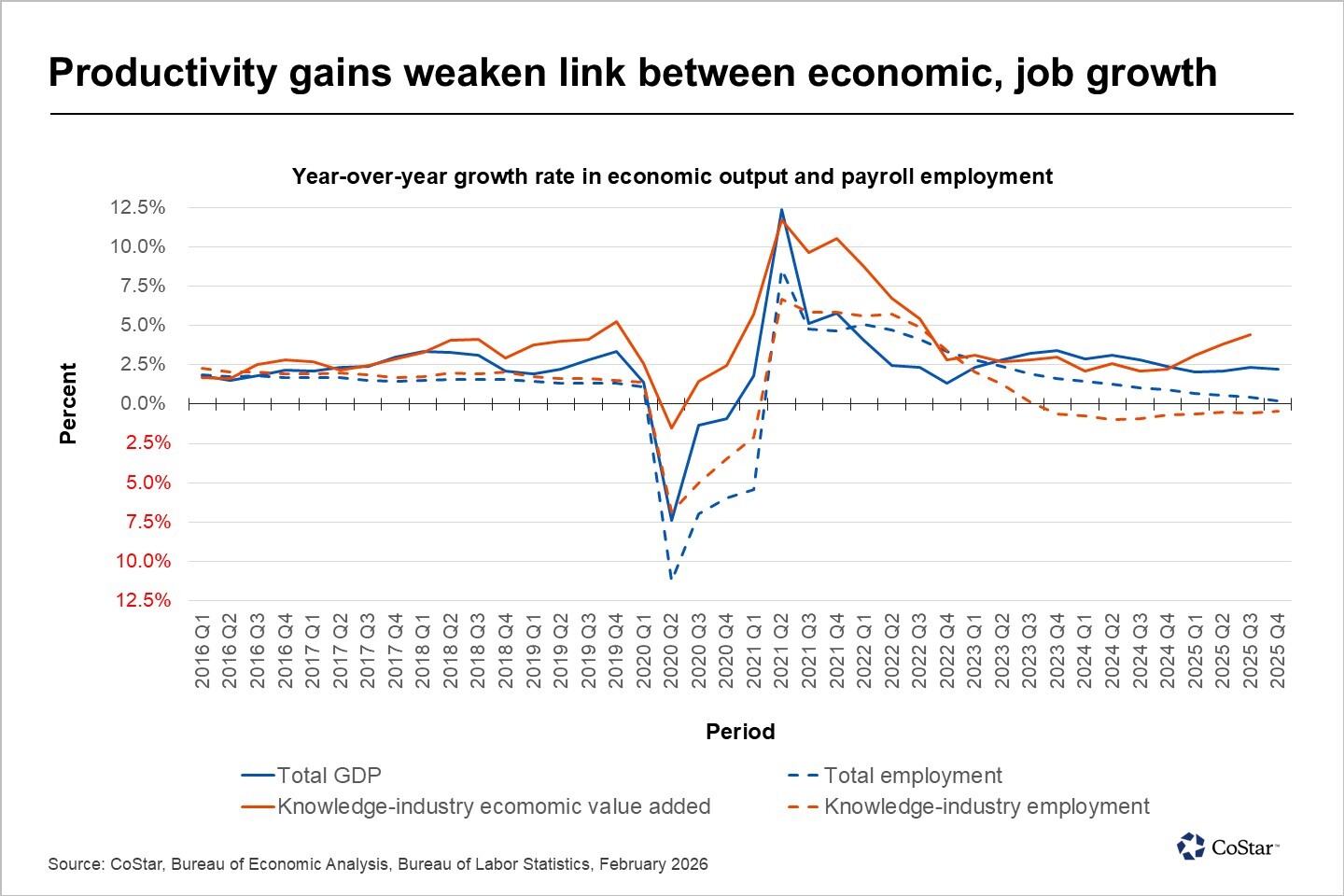

The longstanding relationship between economic expansion and job growth has begun to fray, especially among traditionally office-hungry industries. Should this trend continue, it may well represent another structural headwind to long-term demand for office space.

Labor productivity increased dramatically in 2025. Gross domestic product, or GDP, increased at a rate roughly between 2.0 and 2.5%, while job growth continued to decelerate to a rate barely above zero by the end of the year.

Capital investment and productivity drive the disconnect between jobs and GDP growth

This trend of increased productivity and lower job growth was even more pronounced in the traditional knowledge-oriented industries of information, financial activities and professional and business services. Moreover, it was evident much earlier.

According to data from the Bureau of Economic Analysis for the third quarter, the most recent available for sector-level data on economic value added, these industries posted a combined year-over-year increase in real output of 4.4% even as payroll employment fell by 0.5%.

The gap between knowledge-industry economic and job growth has been widening since at least the second quarter of 2023, when the number of workers employed by firms in these sectors reached its peak. In the 27 months since then and the end of the third quarter, these firms have collectively increased their economic value added by a cumulative 7.8%. Meanwhile, they have reduced payrolls by over 600,000 jobs, or nearly 2%.

This is an unprecedented pattern that strongly diverges from the previous 27-month period, which saw payrolls rise nearly 8% and economic growth increase by 12.5%. Since the recovery from the pandemic led to unusually strong growth, the period from mid-2017 through the end of 2019 may provide a better comparison. During that time, economic output from the knowledge industries increased by almost 10%, while payrolls grew by just under 4%.

GDP growth is expected to exceed job growth; in fact, it is necessary if workers are to achieve real wage growth. A more productive workforce enables the typical standard of living to increase.

However, large spikes in productivity can be disruptive to workers in segments of the economy that may suddenly need far fewer of them to produce what the market demands. Historically, this has happened most frequently in blue-collar industries, including agriculture and manufacturing, as machinery and automation delivered substantial productivity gains while eliminating the need for large numbers of workers.

Now, automation and reimagined workflows enabled by artificial intelligence could predominantly affect white-collar jobs. Depending on the speed and magnitude of this impact, companies may find they need both fewer workers and less office space. The potential threat from AI would be another complication for an office industry still adjusting to lower overall attendance and the prospect of future job growth already constrained by population demographics.

It should be noted, however, that this analysis does not necessarily capture the actual productivity gains occurring within the knowledge-oriented labor force. One reason is that some industry employers, such as big technology firms, have been investing heavily in the physical infrastructure required to deploy AI-based tools and services. This investment, which has relatively little reliance on input from white-collar workers, has certainly contributed to economic growth.

Even so, the trend bears close attention. It could be an early indication of an AI-driven transformation of the white-collar labor force — and another disruption in how organizations use office space.